If you are a current homeowner in the Cape, you have likely experienced increased premiums since Hurricane Ian. However, if you are trying to buy or sell, insurance can become a whole different nightmare—for buyers AND sellers.

Let’s break this down a bit.

Quick note: Every insurance premium in this article is an example, not a quote. Eligibility, coverage, deductibles, flood requirements, and pricing can vary dramatically by carrier, property condition, roof, location, prior claims, loan type, and policy details. The point is simple: get written insurance quotes early—before you fall in love with a house.

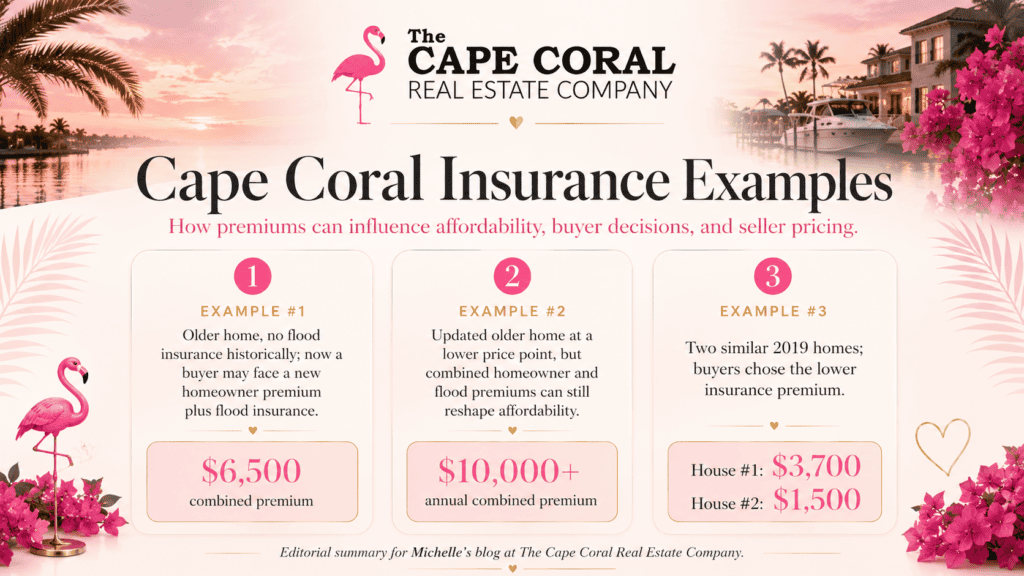

Example #1

Mr. Seller has been in his modest home since 2002. He has homeowner’s insurance, it has never lapsed, and he pays in full each renewal period. His current premium is about $2,500.

He does not carry flood insurance because he owns the home free and clear, and when he purchased it, flood insurance was not required by a lender. His price point is about $475,000.

Mr. Seller’s home is now more than 20 years old. For a buyer to place a new policy on the home, a 4-point inspection will often be required by the insurance carrier. This gives the carrier a clear picture of the age and condition of four key components: roof, electrical, plumbing, and HVAC.

This is not a “nice to have.” It can be a major part of whether a buyer can obtain coverage at a price they can afford.

Now Mr. Buyer’s new policy is already going to be more expensive than the seller’s existing policy. It may also be based on original plumbing and electrical, a 15-year-old roof, and a 10-year-old HVAC system. On top of that, flood maps and underwriting requirements may have changed since the seller bought the home.

An illustrative new homeowners and flood premium? Around $6,500.

Example #2

Mrs. Seller has a beautifully remodeled older home with a new roof, updated electrical and plumbing, and new HVAC. There is absolutely nothing to do except move in.

This price point is well below the average for many Cape Coral single-family homes, at about $300,000. In fact, this would be great for a first-time homebuyer OR someone looking to downsize.

But Mrs. Seller currently pays just over $10,000 per year for her homeowners and flood premiums combined.

Example #3

Mr. and Mrs. Buyer are choosing between two nearly identical homes. The layout and square footage are the same, both have solar, both homes were built in 2019, neither requires flood insurance with the loan they are considering, and both are priced similarly.

The difference? House #1 has a roof type and insurance profile that produces a much higher quote than House #2.

House #1 has more updates and is move-in ready. But Mr. and Mrs. Buyer still chose the home with the lower premium.

House #1 insurance quote: $3,700.

House #2 insurance quote: $1,500.

Are any of these examples the seller’s fault? Nope.

Are any of these examples going to affect the buyer? Absolutely.

Are any of these examples going to affect the seller? Also, absolutely.

Why?

Because any GREAT agent is going to advise buyers to consider the future salability of a home before they even buy it.

Experienced agents, along with the lender writing the loan, can crunch the numbers to determine the effect on affordability and DTI (debt-to-income ratio). Insurance costs can AND DO prevent buyers from being able to afford a home.

Imagine a buyer in a $300,000 price point qualifying for the mortgage…then learning that the insurance is more than $10,000 per year?

Listing agents will guide their clients to price their homes accordingly, because a home is only worth what a buyer is willing to pay. Higher insurance costs can drive buyers toward more affordable options, requiring sellers to lower their asking price.

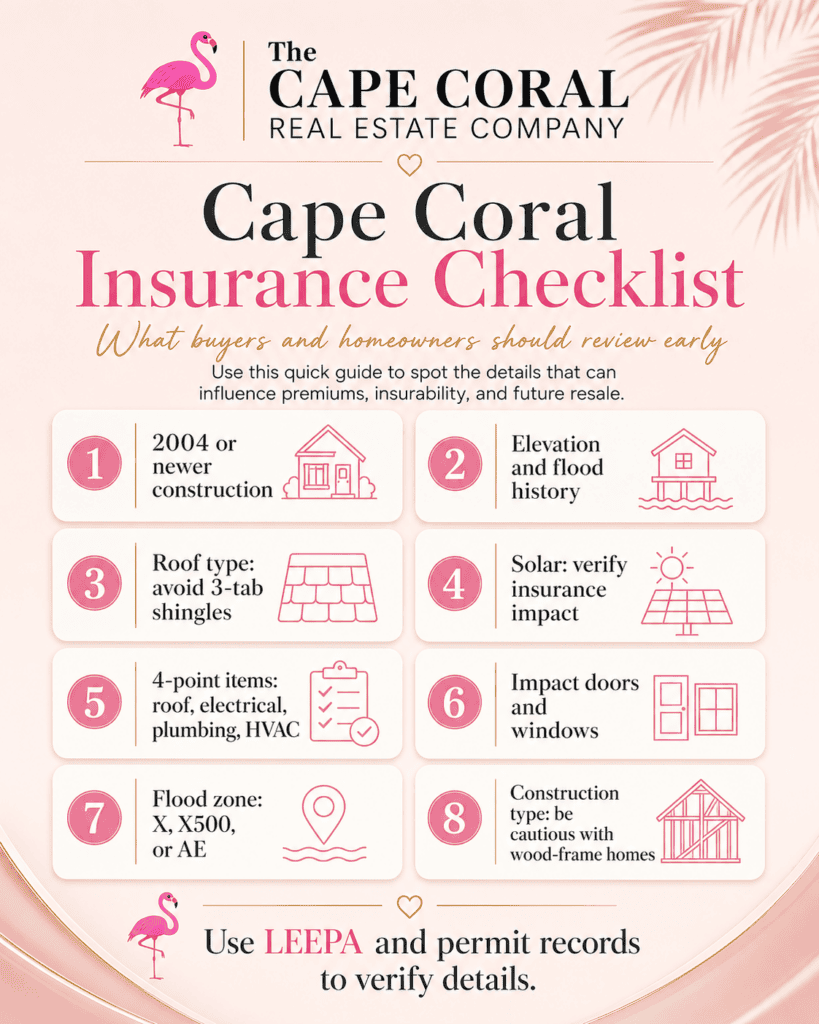

So, As a Buyer in Cape Coral, What Can You Look For?

Homeowners, pay attention too, because some of these items may help lower your premium OR make your home more attractive to future buyers.

1. Start With the Construction Year—But Do Not Stop There

Homes built after the statewide Florida Building Code went into effect may be a better starting point because they were built under more modern statewide standards.

However, the build year alone is not enough. Roof age, impact protection, permits, updates, condition, elevation, and carrier guidelines still matter.

2. Look Beyond the Flood Zone

Do not assume a property is safe from flood risk just because it is in an X zone. And do not assume an AE zone is automatically a deal breaker.

What matters is the complete picture: the flood designation, elevation, prior claims, current flood quote, and your specific lender requirements.

Also, flood zones and evacuation zones are NOT the same thing.

3. Pay Attention to the Roof

Do not get hung up on a roof label alone. Look at the roof age, condition, product, available documentation, permits, wind-mitigation features, and the actual insurance quote.

A roof that looks fine from the driveway may still create a very different insurance result than a buyer expected.

4. Solar Can Add Questions

Solar is not automatically bad. But it can create more questions.

Is it owned, financed, or leased? Was it permitted? How old is the roof underneath it? Does the insurance carrier have special requirements? Are there transfer or payoff obligations?

I will get into more detail in a future article about solar—from real estate and lending to hidden costs. But I would never rely only on what a seller or salesperson says. Get the documents. Get the quote. Read the agreement.

5. Use Public Records as an Early Research Tool

No one expects you to inspect a home during your first walkthrough. But there is basic information you can often find before you fall in love.

The Lee County Property Appraiser and local permit-search tools are great starting points. Search the address, review parcel details, and look for available building and permit history.

You may find permitted bedrooms and bathrooms, square footage, year built, roof permits, HVAC replacements, window updates, pools, fences, and more.

But remember: public records are a screening tool—not a replacement for a 4-point inspection, wind-mitigation inspection, seller documentation, or insurance underwriting.

6. Impact Doors and Windows Matter

When available, impact doors and windows are worth serious consideration.

They can provide peace of mind, energy benefits, and possible insurance advantages. But to receive applicable insurance credit, the openings and installation must be documented and verified correctly.

7. Learn the Difference Between Flood Zones and Evacuation Zones

A, B, C, D, and E are commonly used as hurricane evacuation zones in Lee County.

For insurance purposes, pay attention to the FEMA flood designation for the actual property. In Cape Coral, you may commonly see X, shaded X, AE, and other designations depending on the location.

AE does not automatically mean “bad.” I live on a Gulf-access canal with a transferable policy that costs about $800 per year. I have also seen much higher premiums on dry lots.

Do not avoid a property just because of an AE designation. Ask questions. Get the elevation information. Get the actual quote.

8. Get a Quote Early on Wood-Frame Homes

Wood-frame construction can affect available carriers and premiums in some situations.

That does not mean every wood-frame home is a bad purchase. It means you should get a quote early and understand exactly what you are buying.

And yes…Three Little Pigs 😉

These are the main items to consider.

If you have questions about your own house or a house you are interested in, I am always happy to chat if you do not have an agent who is already working hard for you.

I really do consider myself an advocate, and I spend a great deal of time talking buyers out of potentially costly ventures.

What I can be certain of is that every single one of my clients is well-informed to make a sound decision.

I am not a pushy salesperson. I am passionate about my field and my city. I am also extremely knowledgeable.

But what good is knowledge if we do not share it?

HELPFUL RESOURCES

- Cape Coral Flood Protection Information

- Cape Coral Forerunner Flood Risk Portal

- Cape Coral Flood Zone Maps

- Cape Coral Flood Zone Designations

- Lee County Property Appraiser

- Elevation Certificates

- Florida Wind-Mitigation Info

- Florida Office of Insurance Regulation

- FEMA Flood Map Service Center

RELATED READING

Read Part One: What REALLY Changed the Cape Coral Real Estate Market After Hurricane Ian?

Thinking about buying or selling in Cape Coral?

Contact Michelle for a property-specific strategy conversation.