We’ve all seen headlines that range from “fastest-growing city” to “worst market in America.” It can’t possibly be both! Or can it?

I aim to share insights from my experience in the real estate and lending industries. I don’t just hold a license; I make my living in this industry. As someone deeply involved in both sectors for more than fifteen years across four states, I know it incredibly well. I’m also one of those rare people who LOVE numbers.

Let’s start with something many people point to first: interest rates.

Interest rates absolutely matter. They affect buying power nationwide. But they do not fully explain our current buyers’ market in Cape Coral. The entire country has been dealing with the same rate environment, while our local market was hit with challenges that were very specific to Southwest Florida.

Let’s call rates part of the icing—but they were not the whole cake.

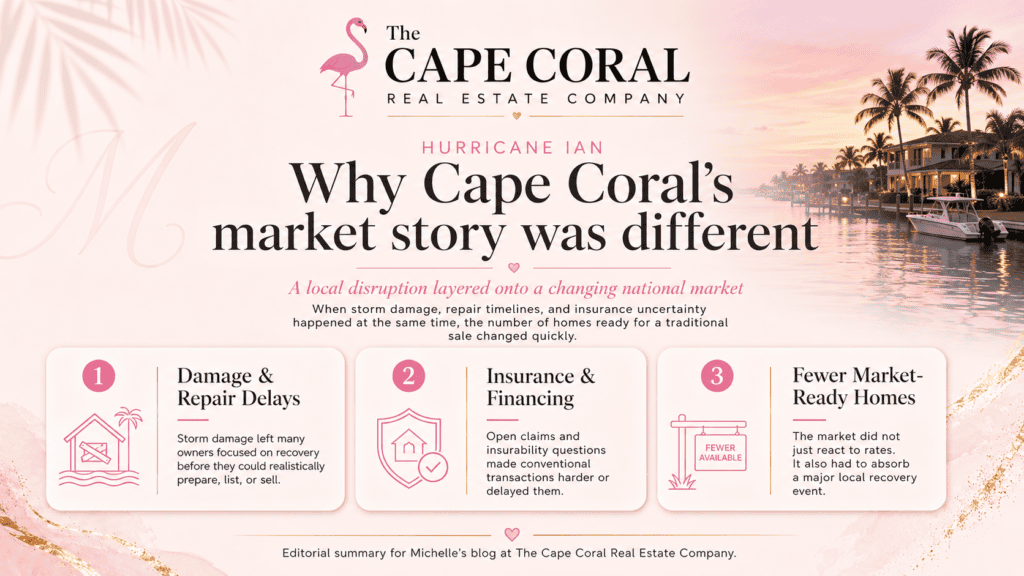

So, what happened almost four years ago that was specific to our area???

Hurricane Ian — September 28, 2022

Hurricane Ian, in my opinion, was one of the first major local strikes against our market. Today, I want to focus on what it did to the number of market-ready single-family homes during that period.

Single-Family Home Closings

Before Hurricane Ian — January 1 through September 28

- In 2021, Cape Coral had 5,085 closings.

- In 2022, Cape Coral had 4,902 closings.

That was a year-over-year decrease of only about 3.6%.

After Hurricane Ian — September 29 through December 31

- In 2021, Cape Coral had 1,884 closings.

- In 2022, Cape Coral had only 869 closings.

That was a year-over-year decrease of about 53.9%.

Data source: FloridaRealtors.org

One can argue that there was already a decline before Hurricane Ian. But the difference after the hurricane was extreme. In my opinion, this is where the local disruption began, and it helps explain why Cape Coral was hit so hard.

Think of all the damage—from cages and roofs to flooding and total destruction. Then think about an entire county of people who needed the same contractors, building materials, inspections, and resources at the exact same time.

Many homes could not be sold traditionally until damage was repaired, insurance questions were resolved, or the home was once again financeable and insurable. Of course, a damaged home could still be sold—but often with known damage, closer to land value, or to a cash buyer who would likely pay far less than the home was worth before the storm or once repairs were complete.

So, most of the community took the time needed to have their homes made whole again. Sadly, many people are still living with damage, but that is an article for a different day.

For homeowners who had the money to begin repairs immediately, the process often moved more quickly than it did for those waiting on insurance. My own example: I paid more than $250,000 out of pocket to get the ball rolling on repairs so I would not have to wait in line with thousands of people who needed the same services.

Even though I hired our initial contractor before noon the day after the storm—while I was still in Miami, without knowing the full extent of our home’s damage, and after assuring him I would pay cash—our home was not “made whole” until October 2023…almost 13 months later.

The 2023 numbers are harder to compare cleanly because our MLS created new statuses that were not previously available, including known damage and land value. The important question is this:

What happens to a volatile market when a community is still piecing itself back together?

What happens when buyers are hesitant after watching a monster like Hurricane Ian take our community by storm?

What happens when sellers cannot move forward because of damage, open insurance claims, repairs, or uncertainty?

What happens when visitors go elsewhere because beaches, restaurants, attractions, and amenities are unsafe or inaccessible?

What happens when short-term rentals are less available because homeowners and out-of-state contractors need places to stay?

THIS is why I believe the market correction reached Cape Coral earlier and hit us harder and FAST.

Interest rates, affordability, insurance costs, new construction, and changing buyer demand all matter. But Hurricane Ian changed the local equation in a way national headlines alone cannot explain.